Interest Only Mortgage Calculator & Guide To Interest Only Mortgages in New Zealand

Use this calculator and guide on how to get an interest-only mortgage in New Zealand.

Interest Only Mortgage Calculator

The Interest Only Mortgage Calculator

investment consultant business

derivative cryptocurrencies investment

real estate real estate investing coaching

chartered accountant for tax filing

business management consulting firm

Property investors love an interest-only loan. A whopping 40% of investors utilise them, compared to a mere 0.5% of owner-occupiers.

But interest-only loans, while cheaper in the short term, are much more expensive over their lifetime.

In this article, you’ll learn why seasoned property investors find interest-only loans so appealing and you’ll be able to use our Interest-Only Mortgage Calculator to see how one could work for you.

Introduction

What Is An Interest-Only Mortgage?

An interest-only mortgage is a temporary loan structure whereby the borrower only pays the interest on the loan and doesn’t pay any of the principal mortgage back.

Interest-only loans are popular with, and used primarily by, property investors to temporarily decrease the size of their mortgage repayments. This saves on costs and increases immediate cash flow.

However, over their lifetime, interest-only loans are more expensive than principal and interest loans (P+I).

This is because every payment you make on a principal loan decreases the amount left, which in turn means less interest.

This is not the case for interest-only loans. But that doesn’t mean they don’t have their place. We generally recommend that investors use interest-only loans for as long as possible, in some cases up to 20 years and beyond.

Who can get an interest-only mortgage

Who Can Get An Interest Only Loan?

Generally, only property investors can get an interest-only mortgage.

The bank will approve an interest-only loan for an owner-occupier in special situations. For instance, if you’re building, or temporarily have two mortgages at once while you move house (what’s known as bridging finance).

But, while most investors can get an interest-only loan, it’s not enough to go to the bank and say: “I’m investing in this property and I want an interest-only loan to increase my cashflow”.

You need to have a valid reason.

Often this is as simple as it’s more tax efficient to use an interest-only loan, rather than go and principal and interest. Here at Vince Money Group, our Accounting division can provide you with a letter to explain that to the bank if necessary.

Loan Lengths

How Long Can I Get An Interest Only Loan For?

The phrase “interest-only mortgage” is a bit of a misnomer. Because when you apply for one, you’re really approved for a 30-year principal and interest mortgage with a 5-year interest-only period.

But, at the end of that 5-year period, your loan will move to principal and interest by default.

However, there is nothing stopping you from applying for another 5-year period, lengthening the entire period out to 10 years.

This can start to become difficult if you keep doing this with the same bank. Why?

Because the bank will test your income to see if you can afford to pay off the loan in the remaining period.

Here’s a simple example. Let’s say you apply for a 30-year loan with a 5-year interest-only period. The bank will test your application to see if you can afford to pay off the loan in the remaining 25 years.

Then, when your mortgage is about to roll into a 25-year principal and interest mortgage and you reapply the bank will test you to see whether you could afford the remaining 20 years.

Do the same thing 5 years later, and you’ll be tested over 15 years.

And so on.

This starts to get tough from an income perspective, which could result in your interest-only extension being rejected.

So what are the strategies to get around this?

When you’re applying for your interest-only extension, you can also apply to extend out the mortgage term.

So let’s say you get a 30-year P+I mortgage with a 5-year interest-only period. Once you get to the end of that 5-year period and want to extend, the bank will testing your ability to pay the mortgage over 20 years.

But if you apply to extend the term back to a total of 30 years (with a 5-year interest onlyperiod), then the bank is only testing your ability to pay the loan over 25 years.

Remember too, you can also move between banks. So if one bank won’t approve your interest-only extension, perhaps another bank will.

What Will My Repayments Be?

How Much Lower Will My Repayments Be On An Interest-only Mortgage?

The amount you can temporarily save using an interest-only mortgage depends on the interest rate.

To give an example, let's say you take out a $500,000 loan. Now let’s say the interest rate on this loan is set at 4%, over a 30-year term.

If this was a standard principal and interest mortgage, then the weekly repayment would be $550.50.

However, if the loan was initially put on an interest-only mortgage, the weekly repayment would be $384.62, saving $143.12 per week.

So, if we look at this in terms of the 5-year lifespan of an interest-only period, this saving equates to $43,129.74. This is the sum that would otherwise have been spent paying off your P+I mortgage.

It’s a huge amount.

However, the overall cost of an interest-only mortgage is still higher than a P+I loan because you will face more interest costs. Why? Because as you pay down the principal of a mortgage, your loan size is smaller so there’s less interest cost and more of your payment goes towards paying off the loan.

But with interest-only, because you never pay down the loan, your interest costs don’t start to reduce. And at some point you’ll need to pay back the loan – either when you sell the property or when you begin making principal repayments.

For fun, let’s use the same example as above and compare scenarios of total interest costs.

Scenario 1

You take out a $500,000 loan, and pay it down over 30-years at 4% interest. This incurs $358,778 in interest costs.

Scenario 2

You take a 5-year interest-only mortgage, which turns into a 25 year P+I mortgage, which you then pay off over that time. This incurs $391,165 in interest costs. (+ $32,386.95 more than a P+I loan)

Scenario 3

You take a 10-year interest-only mortgage, which turns into a 20 year P+I mortgage. This incurs $426,568 in interest cost. ( $67,790.40 more than a P+I loan)

As you can see, any scenario of taking out an interest-only loan results in much higher interests costs. In these examples, it’s a substantial $32,386 and $67,790 more for a 5 and 10 year period, respectively.

So, while you are making a large saving in the short term, an investor will have to consider this in terms of the overall balance of things.

Why Use An Interest Only Loan?

What Are The Benefits Of Using An Interest-Only Mortgage?

If we consider significantly higher interest rates over time for a relatively short period of savings, why is it that almost half of investors leap at the opportunity to get an interest-free loan?

The answer is two-fold.

Increased Cash Flow

Firstly, interest-only mortgages significantly improve the cash flow on an investment property.

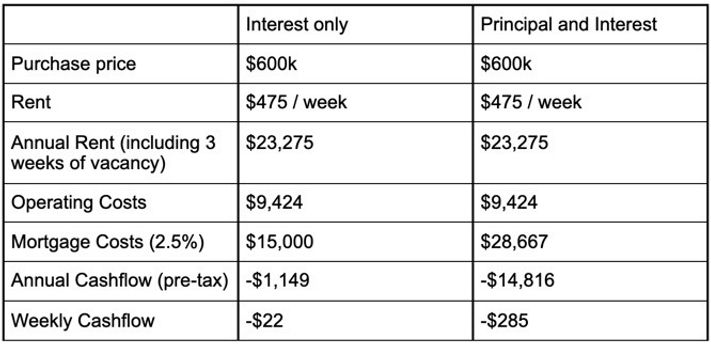

Let’s take an example of a $600k property earning $475 a week in rent and compare the cashflows.

Because the mortgage costs are significantly higher, the property’s cash flow is significantly poorer.

You Don’t Need To Pay Off Debt To Get Ahead

The second reason investors opt for going interest-only is: You don’t have to pay down debt to get ahead.

One of the biggest misconceptions first-time property investors tend to have is you need to pay off your investment mortgage to build wealth.

This is not necessarily true.

When you run the numbers, long-term capital growth creates more wealth than paying down debt.

Let’s go back to the example of the $600,000 property, financing at 100% on a 30-year principal and interest table loan.

Over the first 15 years, you’ll pay off just under $194,000. For that, you’ll invest just under $200,000 worth of cash flow.

And based on a 5% capital growth rate, you would make about $588,000 in capital growth.

All up, you invest $200,000 of cash flow in order to make $782,000. So that’s a 3.91x return on the cash you invested.

On the other hand, if you go interest-only you won’t pay off any debt. But you’ll only invest just over $45,000 in cash flow over the 15 year period. You’ll still get the capital growth – $588,000 which is a 13.07x return on your cash invested (45k for a $588k return).

So, interest-only loans tend to give your properties a better return on the cash you invest, especially in a rising market.

Yes, for sure, you can pay off your mortgage and achieve capital growth at the same time. But what this indicates is real wealth is created by holding assets that increase in value over time.

The other benefit is because they don’t take up as much cash, you can potentially purchase more property.

In the above example, one property on principal and interest would cost $200,000 in cash over 15 years. But 4 properties on interest-only would only cost $180,000 ($45,000 each).

That means getting capital growth on four properties, rather than just one.

It is for this reason why property investors love an interest-only loan.

Because these loans require smaller payments, investors can typically buy more property than if they were to use the alternative P+I.

FAQs

Frequently Asked Questions About Interest Only Mortgages

How Do You Calculate Interest-only Mortgage Repayments?

Calculating repayments is relatively simple. Take the interest rate and divide it by 100, then multiply it by your mortgage amount. This will give you the amount of interest you'll pay in one year.

Then divide that amount by 52 if making weekly repayments, 26 if making fortnightly repayments, or 12 if making monthly repayments.

For instance, if you had a $500,000 mortgage and were paying 4% interest and making monthly repayments:

-

4/100 = 0.04

-

0.04 x $500,000 = $20,000

-

$20,000 / 12 = $1,667 per month

Can You Get An Interest Only Mortgage?

Yes, interest-only mortgages are still available in New Zealand, depending on which bank you talk to. Each bank has different policies, so it is best to talk to a mortgage broker when negotiating your loan.

When you apply for an interest-only mortgage you need to give a reason why you want this loan. For property investors, this can usually be as simple as interest-only loans provide better savings for property investors when they still have a personal mortgage.

How Long Can You Have An Interest-Only Mortgage?

Generally, banks will offer you an interest-only loan for 5 years at a time. At the end of this period, you will have to reapply.

However, this 5-year period is taken off your original loan term. If you have a mortgage with a 30-year loan term and you opt to go interest-only for 5 years, then you need to have the income to pay down the principal over a 25 year period.

Before the banks approve your interest-only mortgage, they will test whether you have the income, right now, to afford the higher payments once the interest-only period ends.

Why Would You Choose An Interest-Only Mortgage?

There are two reasons why an investor would opt to use an interest-only mortgage as opposed to a principal and interest mortgage.

-

Firstly, an interest-only mortgage is significantly cheaper, which means your investment property will require a much lower contribution each week. Therefore, an investor can afford to purchase more properties at one time, building a larger portfolio.

-

Secondly, an interest-only mortgage is much more tax efficient, especially when an investor already has a personal mortgage. This is because an investor can use the money she would otherwise put into the investment property and use it to pay down his personal mortgage.

Other Resources

Use our Mortgage Calculator to calculate a standard table mortgage. Or see our other calculators here.